Alongside the release of the 2026 retirement plan limits and the upcoming implementation of the Roth catch-up provision for high earners…

employers should be aware of several other notable developments affecting the retirement plan landscape. Read on for the key fiduciary updates.

Executive Order on Access to Alternative Assets for 401(k) Investors

Given the amount of headlines and news coverage, it is only natural that plan sponsors and employer plan fiduciaries have questions about the new White House Executive Order on Access to Alternative Assets for 401(k) Investors—and the growing conversation around private market exposure in DC plan investments. Plan advisors can generate significant value by helping their clients separate the buzz from the facts and understand what the Executive Order and related agency action can’t—and can—do.

Executive Action Cannot Change the ERISA Investment Standard

The Executive Order and follow-up Department of Labor (“DOL”) and other agency action cannot–and will not–alter the standard for selecting and monitoring investment options within a plan lineup. This standard is both strict and well-established. Fiduciaries must act solely in the interest of plan participants, with the exclusive purpose of maximizing risk-adjusted returns, net of fees. That principle applies universally, regardless of whether an investment includes public or private market assets.

This means that if a responsible fiduciary conducts a prudent evaluation process that evaluates all of the relevant facts and circumstances, and reasonably determines that a target date fund (TDF) with private market components meets the ERISA standard, that option may be added to the plan.

Executive Action Can Provide Directionally Helpful Commentary

Any ERISA investment decision must be supported by a prudent process that considers all relevant facts and circumstances. Investments with private markets exposure raise unique issues (e.g., liquidity and valuation) that should be evaluated as part of the determination as to whether the investment is reasonably likely to maximize risk-adjusted financial returns, net of fees. The prior Trump Administration DOL issued guidance on such considerations, and it can be expected that the current DOL will issue further guidance in response to the Executive Order.

Advisors will want to continue to monitor these developments, particularly as new asset allocation funds with private market exposure come to market. Regardless of what investment is ultimately selected, advisors should have the expertise to evaluate the available universe of investments, including ones with private market exposure and the unique issues they raise.

Dan Aronowitz Confirmed as Head of EBSA

The U.S. Senate confirmed Dan Aronowitz on September 19, 2025, as Assistant Secretary of Labor, to lead the Employee Benefits Security Administration (EBSA) division of the DOL. Mr. Aronowitz has extensive ERISA and fiduciary liability experience, having formerly been with Encore Fiduciary.

Mr. Aronowitz has expressed a desire to encourage plan sponsors to expand benefits with assistance from the DOL. In our retirement system, whether or not to offer a retirement plan is a voluntary decision by employers. Mr. Aronowitz has emphasized the need to provide regulatory clarity to help well-intentioned employer plan fiduciaries comply with law – and to help eliminate what he described as “ERISA litigation abuse that is turning benefit plans into liability traps.”

There are several areas of focus where DOL may prioritize helping employers gain regulatory clarity, including private market exposure in defined contribution plan investment options, the treatment of participant forfeitures, and the definition of fiduciary investment advice. It will be worthwhile to monitor all such efforts, although it is also important for employer plan fiduciaries and advisors to recognize what cannot be changed by regulatory action. In all circumstances, investment decisions involving ERISA plan assets should be made for the sole purpose of maximizing risk-adjusted returns, net of fees, and a prudent process that takes into account relevant facts and circumstances should support such decisions.

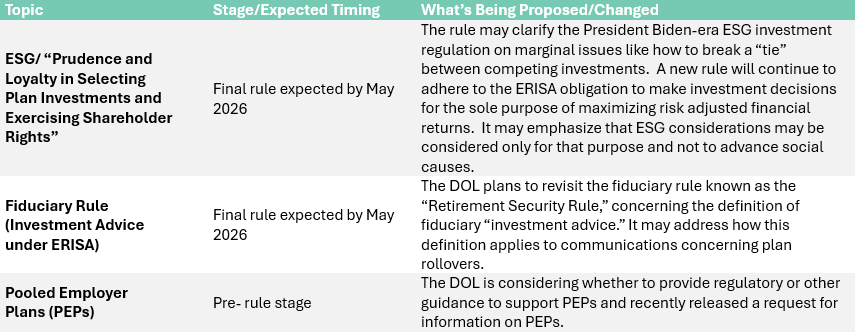

EBSA Regulatory Agenda lists ESG, the Fiduciary Rule, Pooled Employer Plans, and More

DOL’s recently released regulatory agenda has signaled many rulemaking and guidance initiatives from EBSA that may be of relevance to retirement plans and advisors.

Key Items in the Agenda

The table summarizes several noteworthy regulatory initiatives the EBSA has on its agenda, with expected timing and substance. A complete listing is available here.

In all, EBSA’s updated Spring 2025 regulatory agenda lists 20 items and provides an indication of changed priorities under new leadership. As above, these agenda items are worth monitoring but should not alter employer plan fiduciaries’ and advisors’ core and ongoing ERISA compliance activities.